PyCurve : Python Yield Curve is a package created in order to interpolate yield curve, create parameterized curve and create stochastic simulation.

![]()

PyCurve is a Python package that provides to user high level

yield curve usefull tool. For example you can istanciate a Curve

and get a d_rate, a discount factor, even forward d_rate given multiple

methodology from Linear Interpolation to parametrization methods

as Nelson Siegel or Bjork-Christenssen. PyCurve is also able to provide

solutions in order to build yield curve or price Interest rates derivatives

via Vasicek or Hull and White.

Below this is the features that this package tackle :

From pypi

pip install PyCurve

From pypi specific version

pip install PyCurve==0.0.5

From Git

git clone https://github.com/ahgperrin/PyCurve.gitpip install -e .

This object consists in a simple yield curve encapsulation. This object is used by others class to encapsulate results

or in order to directly create a curve with data obbserved in the market.

| Attributes | Type | Description |

|---|---|---|

| rt | Private | Interest rates as float in a numpy.ndarray |

| t | Private | Time as float or int in a numpy.ndarray |

| Methods | Type | Description | Return |

|---|---|---|---|

| get_rate | Public | rt getter | _rt |

| get_time | Public | rt getter | _t |

| set_rate | Public | rt getter | None |

| set_time | Public | rt getter | None |

| is_valid_attr(attr) | Private | Check attributes validity | attribute |

| plot_curve() | Public | Plot Yield curve | None |

from PyCurve.curve import Curvetime = np.array([0.25, 0.5, 0.75, 1., 2.,3., 4., 5., 10., 15.,20.,25.,30.])rate = np.array([-0.63171, -0.650322, -0.664493, -0.674608, -0.681294,-0.647593, -0.587828, -0.51251, -0.101804, 0.182851,0.32962,0.392117, 0.412151])curve = Curve(rate,time)curve.plot_curve()print(curve.get_rate)print(curve.get_time)

[ 0.25 0.5 0.75 1. 2. 3. 4. 5. 10. 15. 20. 25.30. ][-0.63171 -0.650322 -0.664493 -0.674608 -0.681294 -0.647593 -0.587828-0.51251 -0.101804 0.182851 0.32962 0.392117 0.412151]

This object consists in a simple simulation encapsulation. This object is used by others class to encapsulate results

of monte carlo simulation. This Object has build in method that could perform the conversion from a simulation to

a yield curve or to a discount factor curve.

| Attributes | Type | Description |

|---|---|---|

| sim | Private | Simulated paths matrix numpy.ndarray |

| dt | Private | delta_time as float or int in a numpy.ndarray |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_sim | Public | sim getter | _rt |

| get_nb_sim | Public | nb_sim getter | sim.shape[0] |

| get_steps | Public | steps getter | sim.shape[1] |

| get_dt | Public | dt getter | _dt |

| is_valid_attr(attr) | Private | Check attributes validity | attribute |

| yield_curve() | Public | Create a yield curve from simulated paths | Curve |

| discount_factor() | Public | Convert d_rate simulation to discount factor | np.ndarray |

| plot_discount_curve(average) | Public | Plot discount factor (average :bool False plot all paths True Plot estimate) | None |

| plot_simulation() | Public | Plot Yield curve | None |

| plot_yield_curve() | Public | Plot Yield curve | None |

| plot_model() | Public | Plot Yield curve | None |

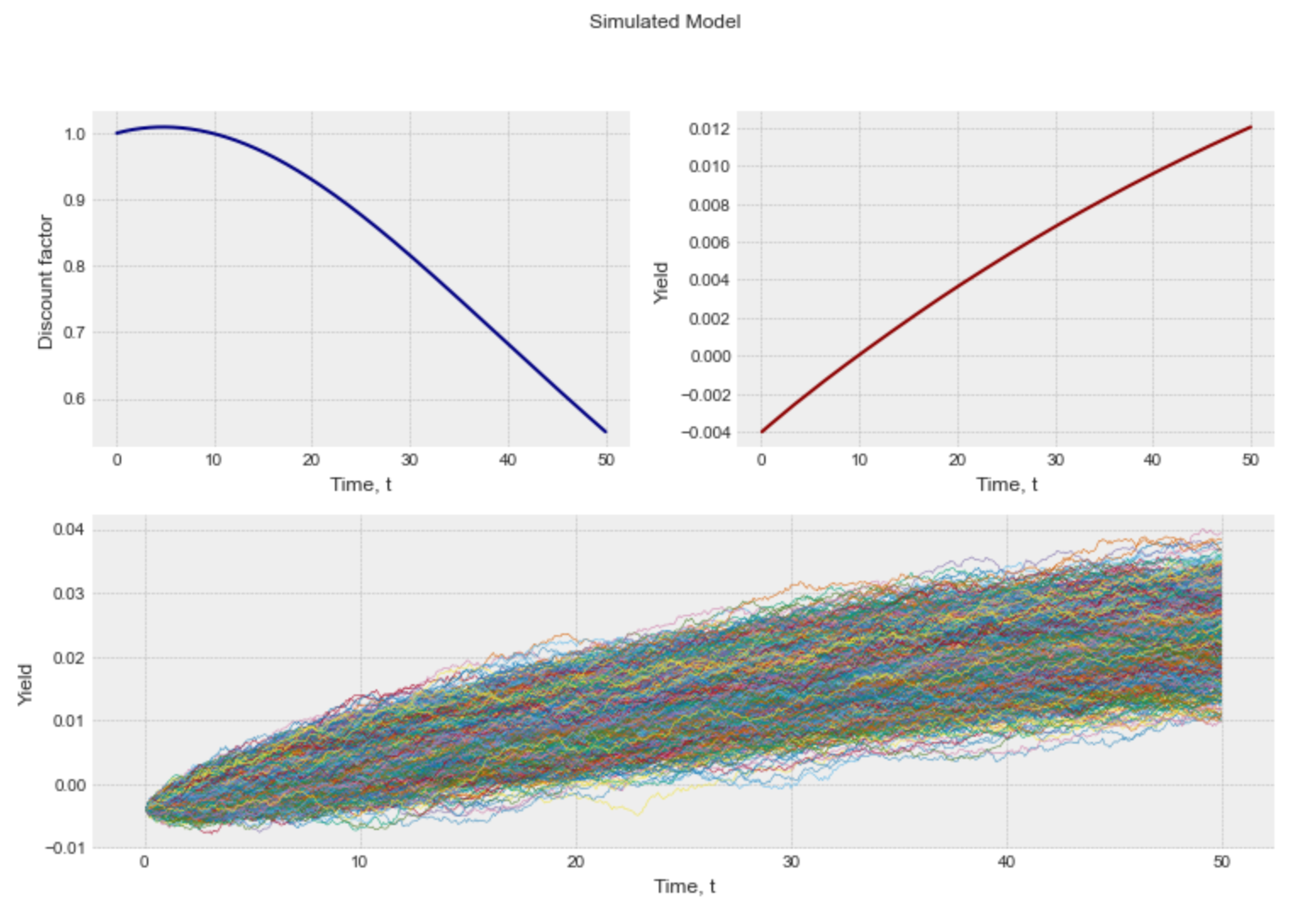

Using Vasicek to Simulate

from PyCurve.vasicek import Vasicekvasicek_model = Vasicek(0.02, 0.04, 0.001, -0.004, 50, 30 / 365)simulation = vasicek_model.simulate_paths(2000) #Return a Simulation and then we can apply Simulation Methodssimulation.plot_yield_curve()

simulation.plot_model()

This section is the description with examples of what you can do with this package

Please note that for all the examples in this section curve is referring to the curve below

you can see example regarding Curve Object in the dedicated section.

from PyCurve import Curvetime = np.array([0.25, 0.5, 0.75, 1., 2.,3., 4., 5., 10., 15.,20.,25.,30.])d_rate = np.array([-0.63171, -0.650322, -0.664493, -0.674608, -0.681294,-0.647593, -0.587828, -0.51251, -0.101804, 0.182851,0.32962,0.392117, 0.412151])curve = Curve(time,d_rate)

Interpolate any d_rate from a yield curve using linear interpolation. THis module is build using scipy.interpolate

| Attributes | Type | Description |

|---|---|---|

| curve | Private | Curve Object to be intepolated |

| func_rate | Private | interp1d Object used to interpolate |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| d_rate(t) | Public | d_rate interpolation t: float, array,int | float |

| df_t(t) | Public | discount factor interpolation t: float, array,int | float |

| forward(t1,t2) | Public | forward d_rate between t1 and t2 t1,t2: float, array,int | float |

| create_curve(t_array) | Public | create a Curve object for t values t:array | Curve |

| is_valid_attr(attr) | Private | Check attributes validity | attribute |

from PyCurve.linear import LinearCurvelinear_curve = LinearCurve(curve)print("7.5-year d_rate : "+str(linear_curve.d_rate(7.5)))print("7.5-year discount d_rate : "+str(linear_curve.df_t(7.5)))print("Forward d_rate between 7.5 and 12.5 years : "+str(linear_curve.forward(7.5,12.5)))

7.5-year d_rate : -0.3071577.5-year discount d_rate : 1.0233404498400862Forward d_rate between 7.5 and 12.5 years : 0.5620442499999999

Interpolate any d_rate from a yield curve using linear interpolation. THis module is build using scipy.interpolate

| Attributes | Type | Description |

|---|---|---|

| curve | Private | Curve Object to be intepolated |

| func_rate | Private | PPoly Object used to interpolate |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| d_rate(t) | Public | d_rate interpolation t: float, array,int | float |

| df_t(t) | Public | discount factor interpolation t: float, array,int | float |

| forward(t1,t2) | Public | forward d_rate between t1 and t2 t1,t2: float, array,int | float |

| create_curve(t_array) | Public | create a Curve object for t values t:array | Curve |

| is_valid_attr(attr) | Private | Check attributes validity | attribute |

from PyCurve.cubic import CubicCurvecubic_curve = CubicCurve(curve)print("10-year d_rate : "+str(cubic_curve.d_rate(7.5)))print("10-year discount d_rate : "+str(cubic_curve.df_t(7.5)))print("Forward d_rate between 10 and 20 years : "+str(cubic_curve.forward(7.5,12.5)))

10-year d_rate : -0.303636605795062710-year discount d_rate : 1.0230694659050514Forward d_rate between 10 and 20 years : 0.6078001168478189

| Attributes | Type | Description |

|---|---|---|

| beta0 | Private | Model Coefficient Beta0 |

| beta1 | Private | Model Coefficient Beta1 |

| beta2 | Private | Model Coefficient Beta2 |

| tau | Private | Model Coefficient tau |

| attr_list | Private | Coefficient list |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| set_attr(attr) | Public | attributes setter | None |

| print_model() | Public | print the Ns model set | None |

| _calibration_func(x,curve) | Private | Private method used for calibration method | float:sqr_err |

| _is_positive_attr(attr) | Private | Check attributes positivity (beta0 and tau | attribute |

| _is_valid_curve(curve) | Private | Check if the curve given for calibration is a Curve Object | Curve |

| _print_fitting() | Private | Print the result after the calibration | None |

| calibrate(curve) | Public | Minimize _calibration_func(x,curve) | sco.OptimizeResult |

| _time_decay(t) | Private | Compute the time decay part of the model t (float or array) | float,array |

| _hump(t) | Private | Compute the hump part of the model given t (float or array) | float,array |

| d_rate(t) | Public | Get d_rate from the model for a given time t (float or array) | float,array |

| plot_calibrated() | Public | Plot Model curve against Curve | None |

| plot_model_params() | Public | Plot Model parameters | None |

| plot_model() | Public | Plot Model Components | None |

| df_t(t) | Public | Get the discount factor from the model for a given time t (float or array) | float,array |

| cdf_t(t) | Public | Get the continuous df from the model for a given time t (float or array) | float,array |

| forward_rate(t1,t2) | Public | Get the forward d_rate for a given time t1,t2 (float or array) | float,array |

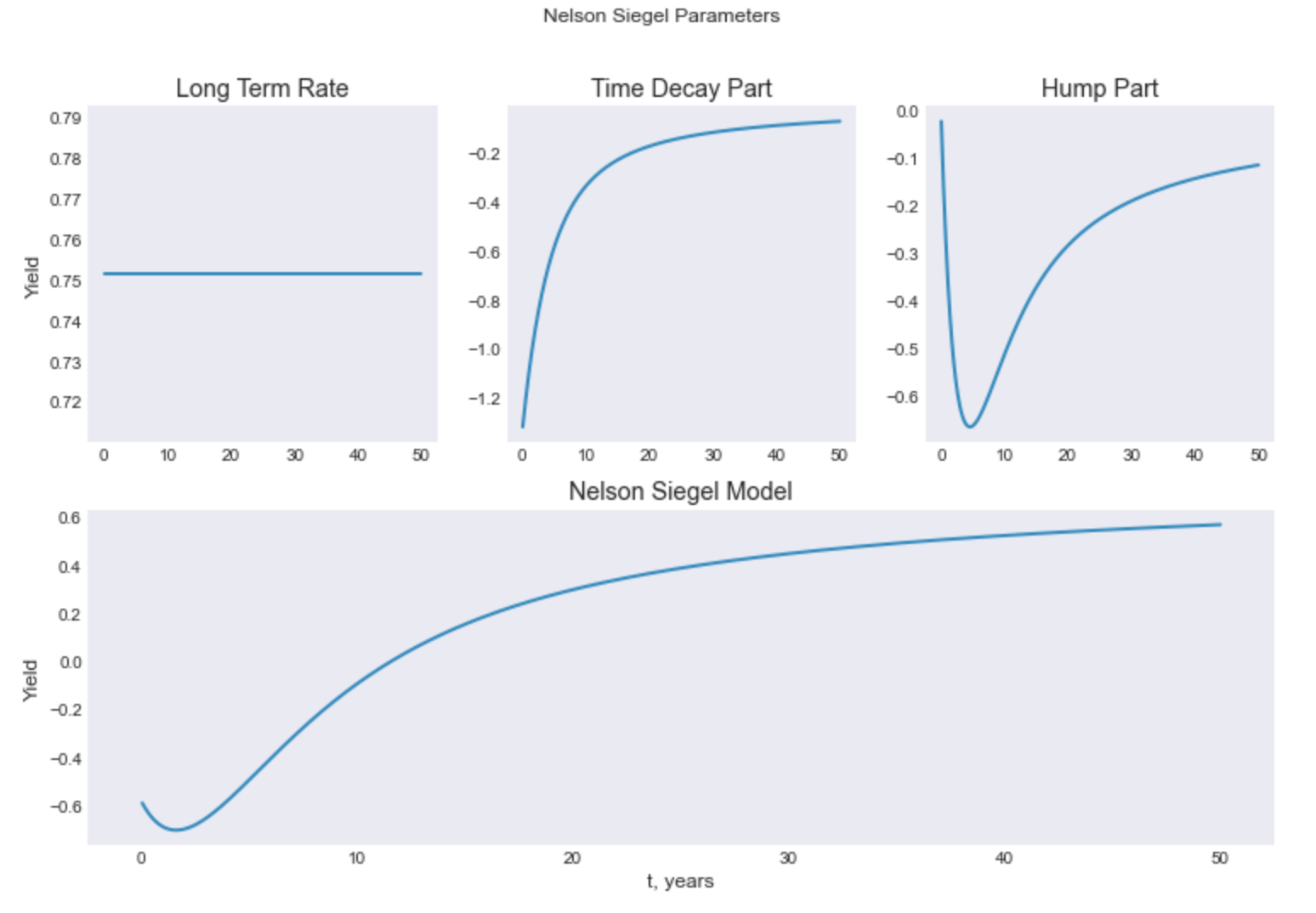

Creation of a model and calibration

from PyCurve.nelson_siegel import NelsonSiegelns = NelsonSiegel(0.3,0.4,12,1)ns.calibrate(curve)

Nelson Siegel Model============================beta0 = 0.751506062319988beta1 = -1.3304971868997248beta2 = -2.2203178895179176tau = 2.5493056203052005____________________________============================Calibration Results============================CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOLMean Squared Error 0.0042367306926415285Number of Iterations 20____________________________Out[19]:fun: 0.0042367306926415285hess_inv: <4x4 LbfgsInvHessProduct with dtype=float64>jac: array([-2.40077054e-06, 9.51322360e-07, -2.33927462e-07, 7.97278914e-07])message: 'CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL'nfev: 105nit: 20njev: 21status: 0success: Truex: array([ 0.75150606, -1.33049719, -2.22031789, 2.54930562])

Plotting and analyse

ns.plot_calibrated()

ns.plot_model_params()

ns.plot_model()

| Attributes | Type | Description |

|---|---|---|

| beta0 | Private | Model Coefficient Beta0 |

| beta1 | Private | Model Coefficient Beta1 |

| beta2 | Private | Model Coefficient Beta2 |

| beta3 | Private | Model Coefficient Beta3 |

| tau | Private | Model Coefficient tau |

| tau2 | Private | Model Coefficient tau2 |

| attr_list | Private | Coefficient list |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| set_attr(attr) | Public | attributes setter | None |

| print_model() | Public | print the Ns model set | None |

| _calibration_func(x,curve) | Private | Private method used for calibration method | float:sqr_err |

| _is_positive_attr(attr) | Private | Check attributes positivity (beta0 and tau | attribute |

| _is_valid_curve(curve) | Private | Check if the curve given for calibration is a Curve Object | Curve |

| _print_fitting() | Private | Print the result after the calibration | None |

| calibrate(curve) | Public | Minimize _calibration_func(x,curve) | sco.OptimizeResult |

| _time_decay(t) | Private | Compute the time decay part of the model t (float or array) | float,array |

| _hump(t) | Private | Compute the hump part of the model given t (float or array) | float,array |

| _second_hump(t) | Private | Compute the second hump part of the model given t (float or array) | float,array |

| d_rate(t) | Public | Get d_rate from the model for a given time t (float or array) | float,array |

| plot_calibrated() | Public | Plot Model curve against Curve | None |

| plot_model_params() | Public | Plot Model parameters | None |

| plot_model() | Public | Plot Model Components | None |

| df_t(t) | Public | Get the discount factor from the model for a given time t (float or array) | float,array |

| cdf_t(t) | Public | Get the continuous df from the model for a given time t (float or array) | float,array |

| forward_rate(t1,t2) | Public | Get the forward d_rate for a given time t1,t2 (float or array) | float,array |

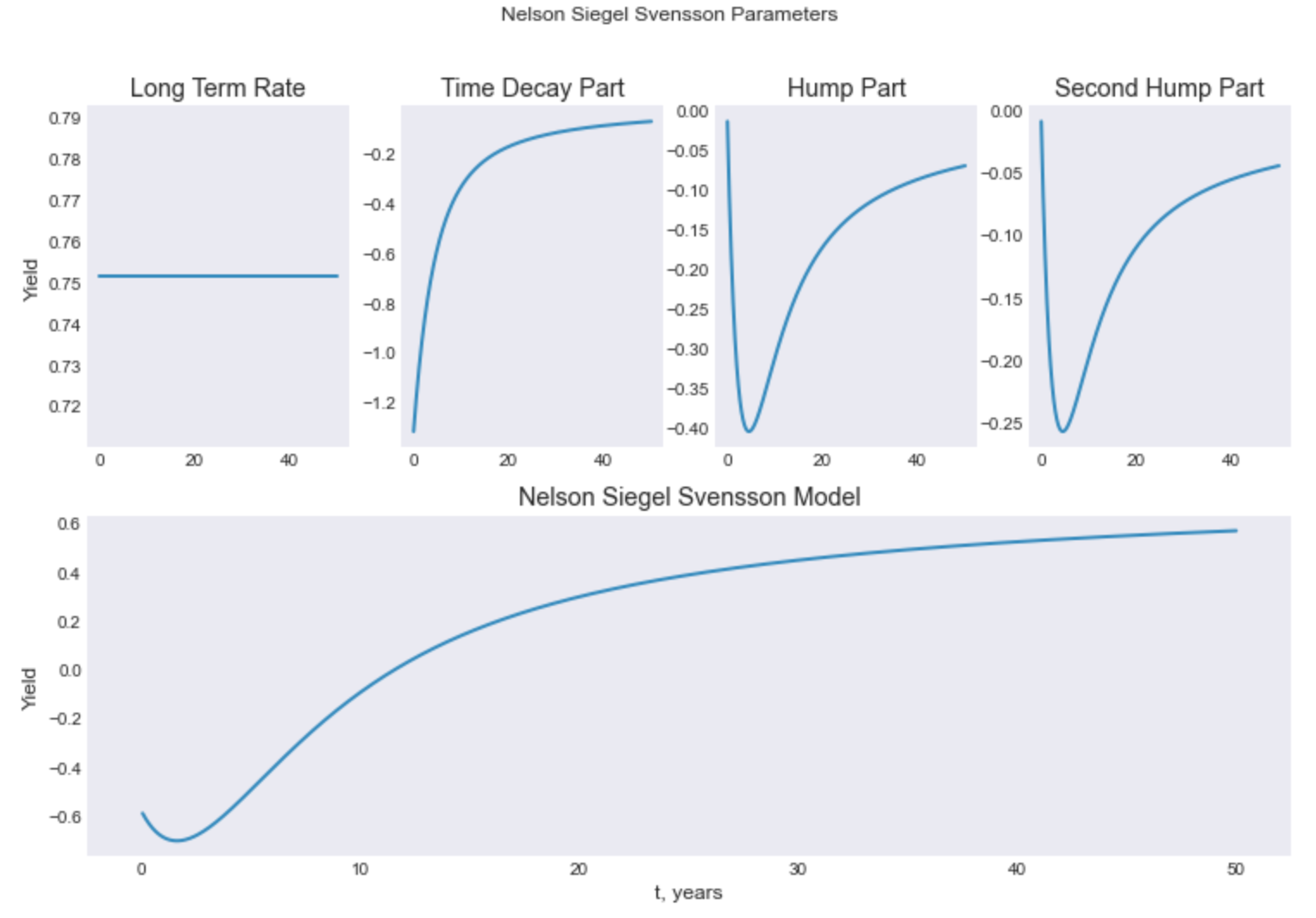

Creation of a model and calibration

from PyCurve.svensson_nelson_siegel import NelsonSiegelAugmentednss = NelsonSiegelAugmented(0.3,0.4,12,12,1,1)nss.calibrate(curve)

Augmented Nelson Siegel Model============================beta0 = 0.7515069899513361beta1 = -1.3304984652740972beta2 = -1.3582175270153745beta3 = -0.8621237370245594tau = 2.5492666085730384tau2 = 2.5493745447283485____________________________============================Calibration Results============================CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOLMean Squared Error 0.004236730702075479Number of Iterations 31____________________________Out[31]:fun: 0.004236730702075479hess_inv: <6x6 LbfgsInvHessProduct with dtype=float64>jac: array([-8.70041881e-06, -3.48375844e-06, -1.71824361e-06, -1.71911096e-06,1.00535900e-06, 3.23178986e-07])message: 'CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL'nfev: 245nit: 31njev: 35status: 0success: Truex: array([ 0.75150699, -1.33049847, -1.35821753, -0.86212374, 2.54926661,2.54937454])

Plotting possibilities are the same as for the Nelson-Siegel model for example

nss.plot_model_params()

| Attributes | Type | Description |

|---|---|---|

| beta0 | Private | Model Coefficient Beta0 |

| beta1 | Private | Model Coefficient Beta1 |

| beta2 | Private | Model Coefficient Beta2 |

| beta3 | Private | Model Coefficient Beta3 |

| tau | Private | Model Coefficient tau |

| attr_list | Private | Coefficient list |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| set_attr(attr) | Public | attributes setter | None |

| print_model() | Public | print the Ns model set | None |

| _calibration_func(x,curve) | Private | Private method used for calibration method | float:sqr_err |

| _is_positive_attr(attr) | Private | Check attributes positivity (beta0 and tau | attribute |

| _is_valid_curve(curve) | Private | Check if the curve given for calibration is a Curve Object | Curve |

| _print_fitting() | Private | Print the result after the calibration | None |

| calibrate(curve) | Public | Minimize _calibration_func(x,curve) | sco.OptimizeResult |

| _time_decay(t) | Private | Compute the time decay part of the model t (float or array) | float,array |

| _hump(t) | Private | Compute the hump part of the model given t (float or array) | float,array |

| _second_hump(t) | Private | Compute the second hump part of the model given t (float or array) | float,array |

| d_rate(t) | Public | Get d_rate from the model for a given time t (float or array) | float,array |

| plot_calibrated() | Public | Plot Model curve against Curve | None |

| plot_model_params() | Public | Plot Model parameters | None |

| plot_model() | Public | Plot Model Components | None |

| df_t(t) | Public | Get the discount factor from the model for a given time t (float or array) | float,array |

| cdf_t(t) | Public | Get the continuous df from the model for a given time t (float or array) | float,array |

| forward_rate(t1,t2) | Public | Get the forward d_rate for a given time t1,t2 (float or array) | float,array |

Creation of a model and calibration

from PyCurve.bjork_christensen import BjorkChristensenbjc = BjorkChristensen(0.3,0.4,12,12,1)bjc.calibrate(curve)

Bjork & Christensen Model============================beta0 = 0.7241026361747042beta1 = 1.2630412759302045beta2 = -4.075775255903699beta3 = -2.61578890758314tau = 2.0454907238894267____________________________============================Calibration Results============================CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOLMean Squared Error 0.002575936865445517Number of Iterations 37____________________________Out[36]:fun: 0.002575936865445517hess_inv: <5x5 LbfgsInvHessProduct with dtype=float64>jac: array([-1.34584183e-06, 7.22165387e-07, -9.63335320e-07, 1.34501786e-06,4.57750160e-07])message: 'CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL'nfev: 252nit: 37njev: 42status: 0success: Truex: array([ 0.72410264, 1.26304128, -4.07577526, -2.61578891, 2.04549072])

Plotting possibilities are the same as for the Nelson-Siegel model for example

bjc.plot_model()

| Attributes | Type | Description |

|---|---|---|

| beta0 | Private | Model Coefficient Beta0 |

| beta1 | Private | Model Coefficient Beta1 |

| beta2 | Private | Model Coefficient Beta2 |

| beta3 | Private | Model Coefficient Beta3 |

| beta4 | Private | Model Coefficient Beta4 |

| tau | Private | Model Coefficient tau |

| attr_list | Private | Coefficient list |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| set_attr(attr) | Public | attributes setter | None |

| print_model() | Public | print the Ns model set | None |

| _calibration_func(x,curve) | Private | Private method used for calibration method | float:sqr_err |

| _is_positive_attr(attr) | Private | Check attributes positivity (beta0 and tau | attribute |

| _is_valid_curve(curve) | Private | Check if the curve given for calibration is a Curve Object | Curve |

| _print_fitting() | Private | Print the result after the calibration | None |

| calibrate(curve) | Public | Minimize _calibration_func(x,curve) | sco.OptimizeResult |

| _time_decay(t) | Private | Compute the time decay part of the model t (float or array) | float,array |

| _hump(t) | Private | Compute the hump part of the model given t (float or array) | float,array |

| _second_hump(t) | Private | Compute the second hump part of the model given t (float or array) | float,array |

| _third_hump(t) | Private | Compute the third hump part of the model given t (float or array) | float,array |

| d_rate(t) | Public | Get d_rate from the model for a given time t (float or array) | float,array |

| plot_calibrated() | Public | Plot Model curve against Curve | None |

| plot_model_params() | Public | Plot Model parameters | None |

| plot_model() | Public | Plot Model Components | None |

| df_t(t) | Public | Get the discount factor from the model for a given time t (float or array) | float,array |

| cdf_t(t) | Public | Get the continuous df from the model for a given time t (float or array) | float,array |

| forward_rate(t1,t2) | Public | Get the forward d_rate for a given time t1,t2 (float or array) | float,array |

Creation of a model and calibration

from PyCurve.bjork_christensen_augmented import BjorkChristensenAugmentedbjc_a = BjorkChristensenAugmented(0.3,0.4,12,12,12,1)bjc_a.calibrate(curve)

Bjork & Christensen Augmented Model============================beta0 = 1.5954945516202643beta1 = -0.1362673420894012beta2 = -1.921347491829477beta3 = -3.100138400789165beta4 = -0.2790540854856497tau = 3.3831338085688625____________________________============================Calibration Results============================CONVERGENCE: REL_REDUCTION_OF_F_<=_FACTR*EPSMCHMean Squared Error 4.6222147406189135e-05Number of Iterations 45____________________________Out[39]:fun: 4.6222147406189135e-05hess_inv: <6x6 LbfgsInvHessProduct with dtype=float64>jac: array([-3.13922277e-05, -1.14224797e-04, -3.47444433e-05, 2.07803821e-05,7.91378953e-06, 6.50288949e-06])message: 'CONVERGENCE: REL_REDUCTION_OF_F_<=_FACTR*EPSMCH'nfev: 357nit: 45njev: 51status: 0success: Truex: array([ 1.59549455, -0.13626734, -1.92134749, -3.1001384 , -0.27905409,3.38313381])

Plotting possibilities are the same as for the Nelson-Siegel model for example

bjc_a.plot_calibrated(curve)

| Attributes | Type | Description |

|---|---|---|

| alpha | Private | Model Coefficient alpha (mean reverting speed) |

| beta | Private | Model Coefficient Beta (long term mean) |

| sigma | Private | Short rate Volatility |

| rt | Private | Initial Short Rate |

| time | Params | Time in years |

| dt | Private | time for each period |

| steps | Private | calculated with dt & time as time/dt |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| sigma_part(n) | Private | compute n sigma part | float |

| mu_dt(rt) | Private | compute drift part | float |

| simulate_paths(n) | Public | Simulate n Short rate paths | np.ndarray |

| plot_calibrated(simul,curve) | Public | Plot yield curve against simulate curve | None |

time = np.array([0.25, 0.5, 0.75, 1., 2.,3., 4., 5., 10., 15.,20., 25., 30.])rate = np.array([-0.0063171, -0.00650322, -0.00664493, -0.00674608, -0.00681294,-0.00647593, -0.00587828, -0.0051251, -0.00101804, 0.00182851,0.0032962, 0.0030092117, 0.00412151])curve = Curve(time,rate)vasicek_model = Vasicek(0.5, 0.0040, 0.001, -0.0067, 30, 1 / 365)simulation = vasicek_model.simulate_paths(200)vasicek_model.plot_calibrated(simulation,curve)

All the tools for graphing from simulation could be applied to vasicek simulation results.

| Attributes | Type | Description |

|---|---|---|

| alpha | Private | Model Coefficient alpha (mean reverting speed) |

| sigma | Private | Short rate Volatility |

| rt | Private | Initial Short Rate |

| time | Params | Time in years |

| dt | Private | time for each period |

| steps | Private | calculated with dt & time as time/dt |

| f_curve | Private | Curve : Initial instantaneous forward structure |

| method | Private | method used in order to interpolate f_curve |

| Methods | Type | Description & Params | Return |

|---|---|---|---|

| get_attr(str(attr)) | Public | attributes getter | attribute |

| _is_valid_curve(curve) | Private | Check if the curve given for calibration is a Curve Object | Curve |

| sigma_part(n) | Private | compute n sigma part | float |

| interp_forward(t) | Private | interpolate forward curve for maturity t | float |

| theta_part(t) | Private | compute theta(t) | float |

| mu_dt(rt,t) | Private | compute drift part at time t | float |

| simulate_paths(n) | Public | Simulate n Short rate paths | np.ndarray |

| plot_calibrated(simul) | Public | Plot yield curve against simulate curve | None |

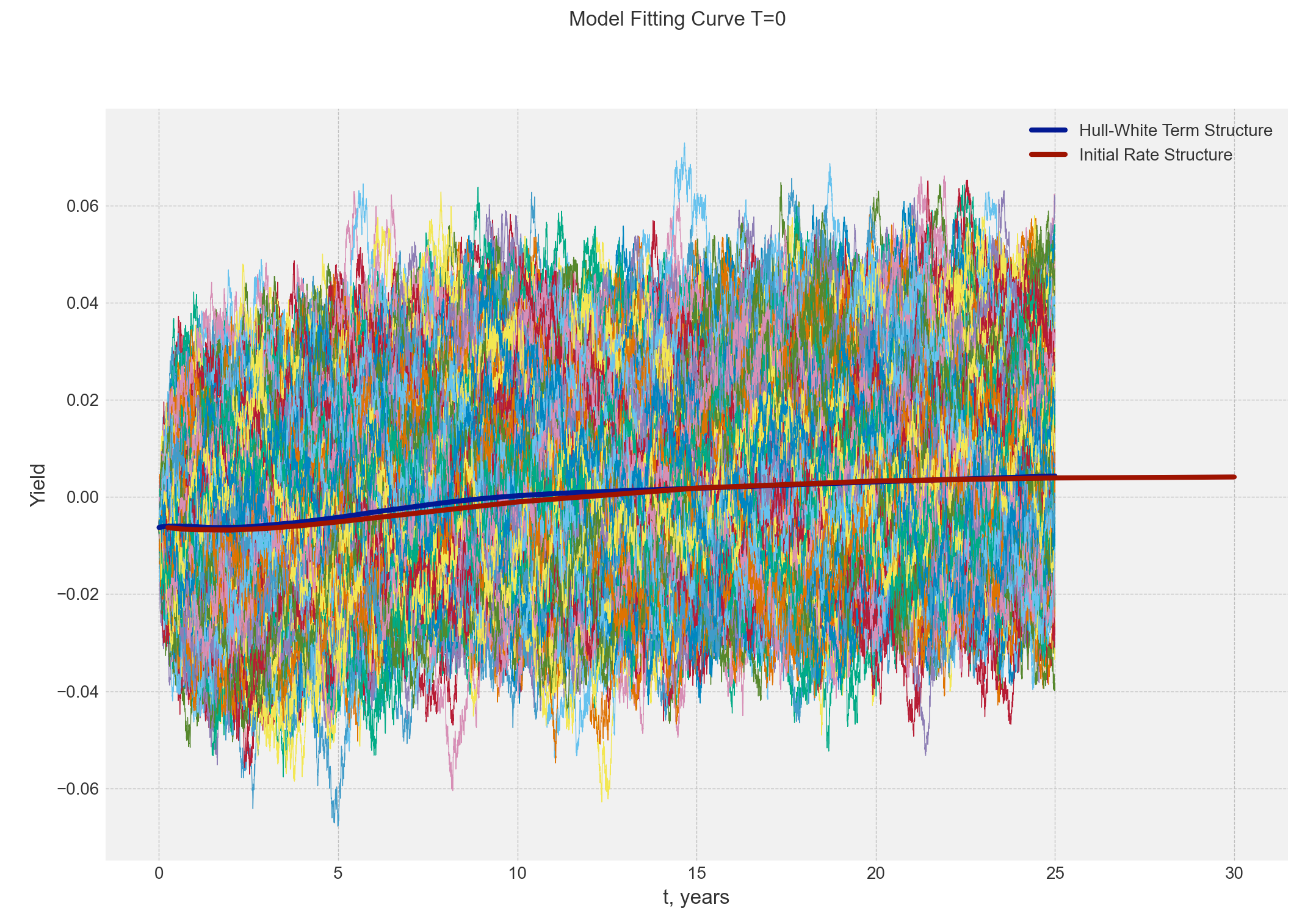

from PyCurve.bjork_christensen_augmented import BjorkChristensenAugmentedfrom PyCurve.hull_white import HullWhiteimport numpy as npfrom PyCurve.curve import Curve# Instance of curve : Spot Ratestime = np.array([0.25, 0.5, 0.75, 1., 2.,3., 4., 5., 10., 15.,20., 25., 30.])rate = np.array([-0.0063171, -0.00650322, -0.00664493, -0.00674608, -0.00681294,-0.00647593, -0.00587828, -0.0051251, -0.00101804, 0.00182851,0.0032962, 0.00392117, 0.00412151])curve = Curve(time, rate)# Deduce Forward rate via Bjork Christensen (as example but you can directly create an instance of Curve with values)bjc_a = BjorkChristensenAugmented(0.3, 0.4, 12, 12, 12, 1)bjc_a.calibrate(curve)forward_curve = [-0.006301821217413436379]forward_curve_t = [0]for i in range(12):forward_curve.append(bjc_a.forward_rate(time[i], time[i + 1]))forward_curve_t.append(time[i])instantaneous_forward = Curve(forward_curve_t, forward_curve)# Hull and white model with High Volatilityhull_white_model = HullWhite(1, 0.02, -0.0063, 25, 1 / 365, instantaneous_forward, 'linear')simulation = hull_white_model.simulate_paths(1000)hull_white_model.plot_calibrated(simulation,curve)

Bjork & Christensen Augmented Model============================beta0 = 0.0003242320890548229beta1 = 0.00042283628067360974beta2 = 0.014729859086888815beta3 = -0.03083749691652102beta4 = -0.020626731632810553tau = 1.137911384276111____________________________============================Calibration Results============================CONVERGENCE: REL_REDUCTION_OF_F_<=_FACTR*EPSMCHMean Squared Error 3.084012924460394e-06Number of Iterations 24____________________________

All the tools for graphing from simulation could be applied to Hull-White simulation results.

# Hull and white model with High Volatilityhull_white_model_low_vol = HullWhite(1, 0.00002, -0.0063, 25, 1 / 365, instantaneous_forward, 'cubic')simulation = hull_white_model_low_vol.simulate_paths(1000)simulation.plot_model()hull_white_model_low_vol.plot_calibrated(simulation,curve)